Imagine a world where your bank helps you better understand yourself, where financial transactions are both frictionless and instant, and where risks are anticipated and averted before they begin. Welcome to the future of banking and finance, powered by Artificial Intelligence (AI) and Machine Learning (ML). These transformative technologies are rapidly evolving the game, reshaping how institutions manage revenue, interact with customers, and scale their investments in a matter of days, not years.

The journey began back in 1955 when Dartmouth math professor John McCarthy first coined the term “Artificial Intelligence.” From this acorn of an idea, an oak tree of innovation has grown, towering over the landscape of every industry, including finance and banking industry. Today, AI and data science are no longer just the subjects of sci-fi novels; they are the propelling force driving leading industries into an unprecedented era of growth and profitability.

Fasten your seat belts because AI adoption across industries is taking off and shows no signs of slowing down. Projected global revenues from AI are set to skyrocket from $81.3 billion in 2022 to an eye-popping $383 billion by 2030, marking a compound annual growth rate (CAGR) of 21.4%. This growth is fueled by a perfect storm of faster processor speeds, decreased hardware costs, and improved access to computing power, all leading to the rapid emergence of innovative fintech companies.

Moreover, thanks to the digital revolution, high-quality datasets are being collected efficiently, offering vast opportunities for learning and prediction. But, in this brave new world, the potential of AI-powered systems is tethered to the strength of the existing data and infrastructure, not to mention the labyrinthine world of financial regulation.

In the financial sector, new AI use cases and algorithms uncovered in a matter of days rather than years.

Markus Lippus

, Data science Lead at MindTitan

Indeed, data science is not just rising within financial and banking institutions; it’s positively soaring. Five key factors are providing the wind beneath its wings: the general advancement of technology, factors particular to the financial sector, the potential for increased profitability, competition on the market, and regulatory compliance. With machine learning, companies are finding new ways to streamline productivity and make shrewd decisions based on insights that would baffle even the sharpest human minds. Today’s intelligent algorithms can pinpoint anomalies and sniff out fraudulent information in mere seconds.

So, welcome aboard the AI and ML express, where the banking and finance industry is being reimagined and reinvented before our very eyes.

Main Application of machine learning in the finance and banking industry:

Cost reduction and process optimization

Fraud detection and Credit Scoring

Fully Automated Customer Service

Is your company ready for AI?

The AI-Powered Digital Age: Potential Value of AI in the Banking and Finance Sector

The banking industry is currently undergoing a critical transformation phase. One of the key elements of this transformation is the emergence of AI-first banks. Financial services companies worldwide are recognizing the importance of adopting AI-first strategies to remain competitive and continue providing superior value to their customers. These institutions anticipate increased revenue at lower cost by leveraging AI, revolutionizing customer engagement through personalization, and improving overall banking experiences.

The ‘AI bank of the future’ is envisioned to offer customers intelligent, highly personalized services, seamless omnichannel journeys, and a more embedded banking functionality within partner ecosystems.

Competitive Advantage:

AI can help banks to create a competitive edge over other traditional banks and newer digital challengers, including neobanks and fintech companies. Leading financial and banking institutions are already leveraging AI for faster loan approvals, biometric authentication, and virtual assistants, thereby improving their customer service and efficiency.

Customer Expectations

As digital-native customers are becoming accustomed to the ease, speed, and personalized service offered by technology, their expectations of banks and financial services firms are rising. An AI-first approach can help banks meet these heightened expectations by enabling highly personalized offers, smart services, streamlined omnichannel journeys, and seamless embedding of trusted bank functionality within partner ecosystems.

Operational Efficiency

AI can optimize the operational efficiency of banks and financial services companies through extreme automation of manual tasks and the replacement or augmentation of human decisions by advanced diagnostic engines in diverse areas of bank operations. This helps in cost-saving, increasing productivity, and achieving the speed and agility characteristic of digital-native companies.

Risk Management and Security

AI can be instrumental in improving risk management and security aspects in banks and financial institutions. It can help in detecting fraudulent activities, enhancing cybersecurity measures, improving financial forecasting, and strengthening customer verification processes.

Regulatory Compliance

AI can help a financial services firms comply with regulatory requirements more efficiently and accurately, reducing the risk of penalties and damage to reputation.

Revenue Growth

AI technologies offer banks and financial institutions the potential to increase revenue at lower cost by engaging and serving customers in radically new ways, with highly personalized and efficient services.

Regarding the financial impact, the potential value of artificial intelligence in the global banking sector is tremendous. According to McKinsey, AI technologies could potentially deliver up to $1 trillion of additional value each year for the global banking and finance industry. This includes increased revenues through personalized services, lower costs through higher automation, reduced error rates, better resource utilization, and new opportunities unearthed from the ability to process and generate insights from large data sets.

Overall, transitioning to an AI-first strategy is imperative for banks and financial institutions to remain relevant and competitive in the digital age, meet rising customer expectations, and overcome challenges on multiple fronts. By leveraging AI, a leading financial institution can innovate faster, build deeper customer relationships at scale, and achieve sustainable increases in profits and valuations.

Detailed Use Cases of AI in the Finance Industry

The global COVID-19 crisis has catalyzed the digital transformation trend, including the incorporation of AI within the financial sector. Recent projections by Business Insider suggest that AI in finance has the potential to save banking and corporate entities as much as $447 billion by 2023.

The application of AI in finance is poised for growth as it aids financial institutions in securing a competitive advantage in two key ways:

Elevation in Efficiency. AI helps to automate and streamline routine banking processes. From customer support through chatbots to anti-fraud detection, AI is steadily making tasks more efficient and error-free. Therefore, AI empowers organizations to minimize expenses and boost productivity, culminating in increased profitability. Another notable benefit is the impact of AI on risk management. By leveraging AI for risk assessment, banks can make more accurate predictions, aiding in better decision-making.

Enhanced Customer Satisfaction. With the advent of AI, a variety of highly personalized product offerings are now accessible to an expanding consumer base. It also enables personalized service to customers, thereby improving customer experience and satisfaction significantly.

There are plenty of real-world case studies of banks successfully leveraging AI. For instance, JP Morgan Chase uses AI to analyze legal documents and contracts faster and more accurately. Similarly, HSBC employs AI for money laundering detection, saving both time and money. In addition, Capital One and U.S. Bank use AI for customer service through chatbots, improving their efficiency and accessibility.

However, while the benefits are substantial, achieving the potential trillion-dollar value impact requires banks to overcome multiple operational and organizational challenges, notably skills gaps and the integration of AI into the wider organization. As such, strategic investment in AI technology, coupled with a commitment to continuous learning and adaptation, will be crucial for banks moving forward.

How AI is reducing costs and increasing operational efficiency

The finance industry is harnessing machine learning to lower operational costs and drive profitability. This field involves both front- and back-office activities across multiple institutions.

Cost Reduction In Insurance

Insurance companies sort through vast sets of data to identify high-risk cases and lower any exposure.

Artificial intelligence is applied to such functions as underwriting and claims processing. One of the key technologies here is the application of Natural Language Processing (NLP) which improves decision-making by analyzing large volumes of text and identifying key considerations affecting specific claims and actions.

With the rise of digital and IoT (Internet of Things), the points of contacts with the insured will become even more numerous.

Another set of factors can be included in the insurance claim evaluation process. For example, an ongoing AI-powered dialogue through bracelets, sensors, etc. leads to a more comprehensive understanding of the insured.

By collecting and analyzing additional data, insurers are able to analyze the habits of their policyholders and offer highly customized products, adapted in real-time to the needs and expectations of their clients.

Operational Cost Reduction Ai In Financial Institutions

To maximize their profitability, banks rely heavily on capital optimization.

Artificial intelligence algorithms can be applied to handle large quantities of data to increase the efficiency, accuracy, and speed of mathematical calculations. Using machine learning, banks can find the best combination of the initial margin-reducing trades at a given time based on the degree of initial margin reduction in the past under different combinations of those trades.

Banks are also looking to apply AI algorithms to back-testing, in order to assess the overarching risk models..

Using a range of financial settings for back-testing reveals unpredictable shifts in market behavior and other trends, leading to better decision-making. A similar approach is often applied to stress testing.

Technological advancements can also help financial institutions by introducing a machine learning approach to minimize the trading impact on prices and liquidity, thereby predicting the market impact of specific trades (and the best timing for such trades). This can ultimately lead to the minimized impact of trading both into and out of large market positions.

Credit Scoring

Front office activities such as credit scoring can be optimized to the extent where many financial decisions are based on wide-scale data analysis.

Lenders have long relied on credit score data to make both private and corporate lending decisions. AI-powered credit scoring tools are designed to speed up lending decisions while limiting incremental risk.

Historically, most financial institutions based their credit ratings on the lender’s payment history. As financial institutions strive to enhance their creditworthiness evaluations and boost loan profitability, they are turning to a myriad of data sources, ranging from mobile phone usage patterns to social media activities. However, it’s worth noting that the types and availability of these data sources can significantly vary between countries due to different regulations and privacy norms. Leveraging such technologies allows for faster and cheaper credit scoring and ultimately makes quality loan assessments accessible to a larger number of people.

In the past years, a number of customer-facing fintech companies have emerged. Using an algorithmic approach, some have applied data analysis to provide credit scores for individuals with ‘thin’ credit files, using alternative data sources to review loan applications rejected by lenders.

Advantages/Disadvantages Of Using Ai In Credit Scoring Models

Potential advantages:

AI allows large quantities of customer data to be analyzed very quickly

Potential cost-reduction of assessing credit risks

Increasing the number of individuals with measurable creditworthiness

Potential disadvantages:

AI can find more complex connections from the data compared to a human analyst and those new patterns can sometimes be complicated to understand

Lack of availability or unreliability of third-party data

How AI is minimizing risk and enhancing security

Artificial Intelligence has made its way to asset managers and trading firms. In addition to R&D, some firms now use machine learning to devise trading and investment strategies. Big data and machine learning help large trading firms to strengthen their risk management techniques by centralizing the risks that arise from various parts of their businesses.

In portfolio management, machine learning algorithms are being applied to spot new signals on price movements and to make more effective and rapid trading decisions.

In the past years, a new generation of quant funds has appeared on the market which use an artificial intelligence unit as part of a larger team to aid the asset manager with portfolio construction. Harnessing the predictive power of data can help funds spot new trends and potentially profitable trades that are outside of the human scope of understanding. For example, Hong Kong-based Aidiya is a fully autonomous hedge fund that makes all of its stock trades using artificial intelligence).

The rise of algorithmic trading in recent years – Image source Aite Group

According to an extensive 2017 study, machine learning likely only drives a minor subset of quant funds’ trades. Quant funds manage on the order of $1 trillion in assets, out of total assets under management (AUM) invested in mutual funds globally in excess of $40 trillion.

There are also a growing variety of vendors that provide Big data services for financial market participants.

Such players could scrape news and/or metadata and enable users to identify the specific features (web pages viewed, etc.) that correlate with the events their customers are interested in predicting.

However, we’re far from AI algorithms continuously outperforming human traders. In March 2018, Bloomberg reported that the index of hedge funds using AI had fallen 7.3 percent the past month, compared to a 2.4 percent decline for the broader Hedge Fund Research index.

How AI is revolutionizing fraud detection and prevention

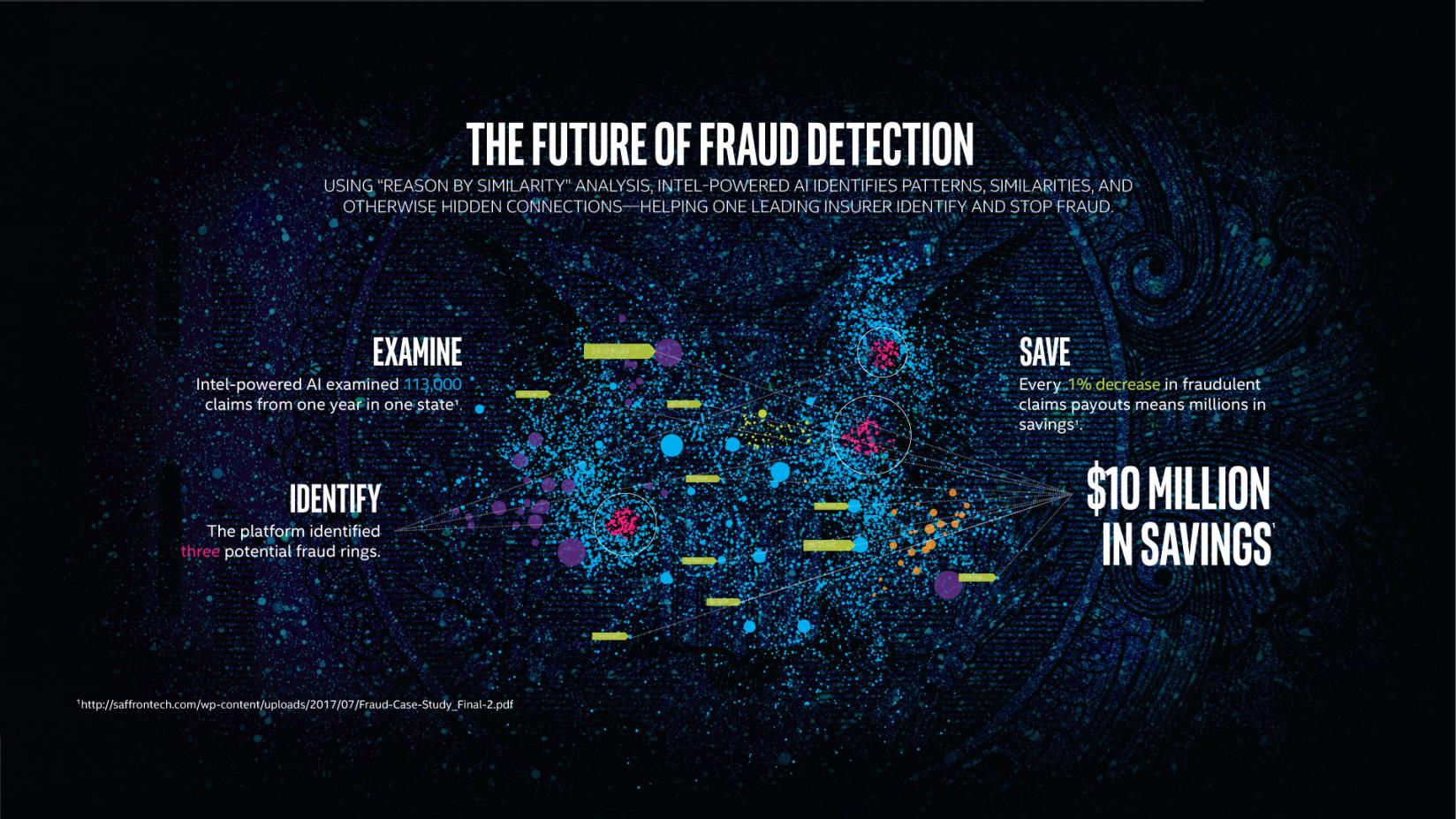

According to an Intel report, the United Nations claims that less than 1% of global illicit financial flows are frozen or seized and that up to 5% of global GDP – $5 trillion annually – are money laundering transactions. Fraudulent claims account for $80-100 billion annually in the U.S. alone.

AI has proven extremely applicable to security and fraud detection use cases. Machine learning algorithms can analyze thousands of data points in real-time and flag suspicious or plain-right fraudulent transactions, stopping many fraudulent claims in the process.

According to Samir Hans, an advisory principal at Deloitte Transactions and Business Analytics LLP,

With cognitive analytics, fraud detection models can become more robust and accurate. If a cognitive system kicks out something that it determines as potential fraud and a human determines it’s not fraud because of X, Y, and Z, the computer learns from those human insights, and next time it won’t send a similar detection your way. The computer is getting smarter and smarter.

Mastercard recently introduced its latest pioneering security platform, Decision Intelligence. The system uses machine learning technology to make data-driven, real-time decisions tailored to the account, including defined alert and decline thresholds. By detecting anomalous shopping spending behaviors, the system can prevent thefts and fraudulent transaction claims.

Chatbots and AI assistants for improved customer experience of banks and financial institutions

Artificial Intelligence (AI) is playing an increasingly significant role in providing personalized banking services, revolutionizing the sector by offering targeted, efficient, and customer-friendly solutions. This is due to AI’s ability to analyze large amounts of data, identify patterns, automate processes, and learn from experience.

Firstly, AI-based systems offer the potential for heightened personalization, tailoring banking services to individual customer preferences and needs. AI can process vast amounts of customer data, identify customer personas, and predict individual customer needs with an increasing degree of precision. This tailoring of banking services not only improves customer satisfaction but can also boost banks’ revenue by better targeting their services to customer needs.

Robo-advisors

Robo-advisors have brought a data-driven and partially automated approach to wealth management systems.

AI-powered tools can provide personalized financial advice and help traders streamline the account opening process, and advise them on scaling their portfolio. This could include developing a financial plan, advising on planned home purchases, retirement, protection needs real estate planning, etc.

The main advantage of robo-advisors is that they are low-cost alternatives to traditional advisors. In the long term, robo-advisor technologies could make financial counselling available to an increasing number of people, resulting in more informed personal finance decisions.

While current robo-advisor total assets under management (AUM) only represent $10 billion of the wealth management industry’s $4 trillion (less than 1% of all managed account assets), Statista estimates that this figure will rise to around $4.66 trillion AUM by 2027.

Machine learning offers a wide array of custom solutions for improving the customer lifetime value and optimizing the sales of financial products.

For example, imagine a recommendation engine capable of suggesting the most suitable insurance package to existing and new customers or identifying new potential users fit for an upselling offer.

By analyzing what makes some customer segments remain loyal customers and others seek out new financial service providers, banks and other stakeholders can target the in-danger segments with motivating offers and products.

Intelligent Chatbots

Another widely popular AI use case (also in the telecom business) are intelligent chatbots.

With some exceptions, AI-powered customer service solutions can be divided into two categories:

Customer service communication

Customer engagement and personalized offers

Custom-built chatbots could be used to streamline large parts of the tedious customer service process, automatically solving simple customer requests and routing others to the right department within the company.

The financial industry, with its large sets of data, is particularly fit for building intelligent customer service bots and systems. To be able to evaluate and resolve customers’ issues accurately, AI algorithms empowering customer communication must process massive amounts of data and interactions.

Regulatory compliance in the financial sector

New regulations have increased the need for efficient regulatory compliance, pushing banks to seek cost-effective means of complying with regulatory requirements. Regulatory technology (RegTech) focuses on making regulatory compliance more efficient and native to a financial institution’s core processes.

Natural language processing (NLP) could be used by asset management firms to cope with new regulations. For example, in the EU, investment managers have to comply with specific requirements in the Markets in Financial Instruments Directive (MiFID II), the Undertakings for Collective Investments in Transferable Securities (UCITS) Directive, and the Alternative Investment Fund Managers Directive (AIFMD). To comply with these regulations, companies can apply AI-powered data analysis to build integrated risk and reporting systems. Moreover, machine learning could help trade repositories (TRs) tackle data quality issues, increasing the value of TR data to authorities and the public. Check out other natural language processing use cases applicable in the financial industry.

Generative AI in banking

Generative AI autonomously generates new content such as text, images, and music by identifying patterns in existing data and new inputs. It employs probabilistic models to create content based on these patterns and defined input parameters. Banks are turning to AI to keep pace with customer demands and overcome operational challenges, such as:

Data Analysis: Enhances decision-making and predictive analytics, boosting efficiency and reducing human error.

Synthetic Data Sets: Improves AI model training while maintaining privacy.

Automated Communications & Reports: Generates customer communications, financial reports, and regulatory documents in real-time, aiding compliance and customer service.

Moreover, generative AI can be used for adaptive fraud detection. Sophisticated AI technologies learn from transaction patterns, enhancing security dynamically. But the most impact AI and LLMs (large language models) can bring to the customer experience in banking, which is crucial for business success in the digital age.

Customer experience (CX) is vital for growth, as highlighted by surveys showing that 87% of leaders view CX as a top growth driver, and 86% of consumers would leave a brand after just two or three bad experiences. AI is seen as a breakthrough technology for achieving personalized and contextual customer experiences. A significant number of bankers (77%) believe that AI will determine banks’ success, and over half (56%) of organizations are already using AI in some capacity.

LLMs and AI can enhance the banking user experience by:

Analyzing customer data for personalized service and real-time support.

Automating routine tasks to improve efficiency and reduce costs.

Providing a conversational banking experience through integrated chat or voice interfaces.

Challenges and barriers to AI implementation in financial institutions

The implementation of artificial intelligence (AI) in the banking sector, while promising tremendous potential value, is not without significant challenges and barriers.

Infrastructure and investment

Many banks have struggled to transition from limited experimental use cases to full-scale deployment of AI technologies across their organizations. A primary cause for this is the lack of a clear AI strategy coupled with an inflexible and underfunded technology core. Indeed, building sophisticated AI systems used to be expensive, necessitating strategic deployment in high-value use cases such as high-frequency trading. While the cost of developing and implementing AI technologies has decreased over time, the financial commitment required remains significant.

Data Challenges

In data science, there’s a saying, “garbage in, garbage out.” This means if we feed poor or biased data into AI, it can cause big problems, like losing money. We need a quick way to spot and fix these data issues. Some companies offer solutions for this by allowing version control for their data, similar to tracking changes in a document.

Data also needs to be tailored for different locations. For global companies, they need to make sure their data makes sense for all the different countries they work in, considering different languages and cultures.

Reducing Complexity in Data

A single transaction can have hundreds of data points. So, banks and finance companies have a lot of data to deal with, which can be overwhelming. When there’s too much data, some machine learning methods have a hard time.

Understanding AI Decisions

In finance, all decisions made by AI need to be understood and approved by the company. For example, if AI determines that someone’s loan application should be denied, the company still needs to explain why. So, while their accuracy makes advanced neural networks attractive, their complexity makes them hard to explain. Other models can be a better fit from the explainability perspective.

Security and Compliance

A major challenge for AI in finance is dealing with the large amounts of customer data collected. This data can be sensitive and needs to be handled carefully. Good data partners offer security options and follow standards to ensure data is handled properly. These include legal and ethical implications arising from the use of AI in customer interactions, loan decision-making, and other banking functions. For example, as AI increasingly forms part of commercial banking processes, concerns about transparency, privacy, and suitable documentation have come to the fore. The application of AI in finance has to align with existing laws and regulations, a challenge that adds a layer of complexity to its integration into the banking industry. As these legal and ethical frameworks continue to evolve, banks must remain adaptable and vigilant.

While AI offers significant potential benefits to the banking sector, its implementation is hampered by challenges related to infrastructure and investment, data and privacy, and regulatory compliance. Overcoming these hurdles will require concerted strategic planning, ongoing investment, careful data management, and a comprehensive understanding and application of regulatory standards.

Conclusion and overview

Every single one of these fields of study is still in its infancy, showing promising advancements, yet far away from complete autonomy from human agents. Looking forward, the future applications of AI in finance and banking industry appear promising, but they come with their own opportunities and challenges. As financial institutions continue to build on their existing AI solutions to solve more complex challenges, AI is expected to revolutionize front-office and middle-office operations, impacting areas such as customer identification, fraud detection, risk management, and regulatory checks.

However, for these advancements to be effective, banks will need to address operational and organizational challenges like skills gaps and the integration of AI into existing structures. Moreover, they will need to invest in creating a robust data infrastructure and tackle potential issues related to data privacy and security. Banks that will succeed in this new era are those that will manage to formulate and execute a holistic AI strategy, leverage partnerships effectively, and remain customer-centric in their approach.

We recommend financial institutions take steps to introduce AI and machine learning to various processes across the company. In the long term, this will benefit the organization both in terms of increased efficiency as well as a competitive advantage.